More of the event here, and my talk should be live soon…

1. Cultural Norms Matter

There’s far less “sharing” in Turkey than in Finland or Sweden. Anyone with a Finnish ID number seems to have access to Supercell’s dashboards! Turkey has largely avoided non-competes, and it must stay that way. King single-handedly has hamstrung Swedish mobile game development with its notorious three-month non-competes, which, after a three-month notice period, amount to six months for an employee to start elsewhere. France is dealing with a similar issue, and it’s to their detriment. Much of Silicon Valley’s success is due to the ban on non-competes, something that’s gone over the heads of subsidy-happy governments.

Matthew Ball’s excellent piece, The Tremendous Yet Troubled State of Gaming in 2024, unpacks a paradox: gaming seems prosperous yet is marred by unprecedented industry layoffs. Ball’s findings reveal a simple reality: playtime is down over 20% (3.5 hours per week) from its COVID peak. This decline, further seen in declining inflation-adjusted spending, cements gaming as an entertainment product with a capped growth potential. Without new strategies to reclaim time to share, gaming’s best days are behind it.

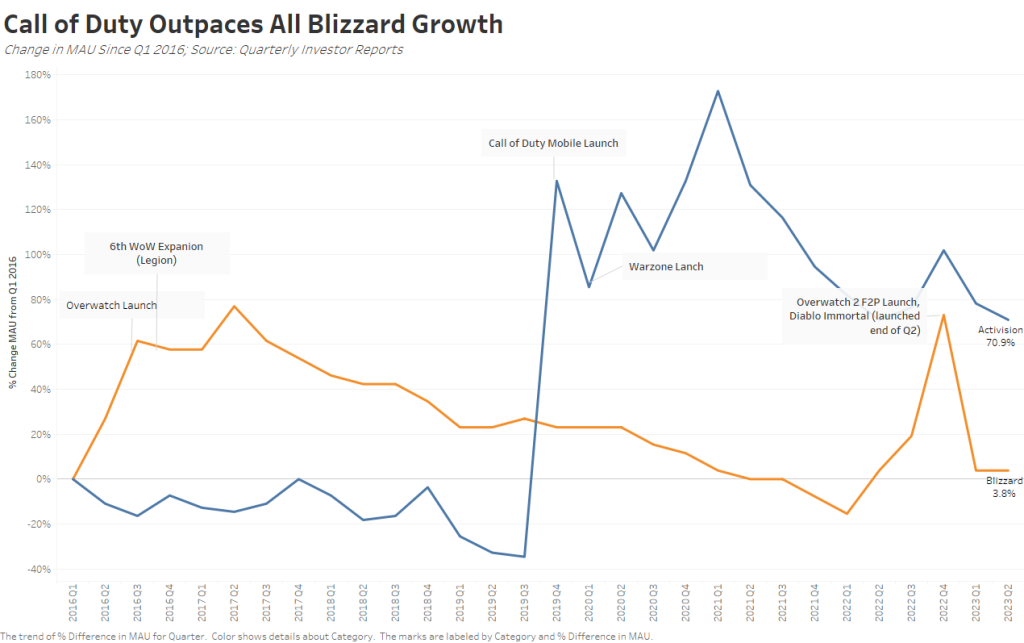

Phil Spencer, Microsoft Gaming CEO, named Johanna Faries the new president of Blizzard, closing a pivotal moment in the ATVI-Microsoft merger. Faries faces the challenge of revitalizing Blizzard amidst declining revenue and engagement across its franchises. The situation is dire enough that Faries inherits a needed rebirth of Blizzard. The Blizzard of old is dead, and several causal agents are responsible.

Ah, web3: a past marked by rug pulls, North Korean heists, and prices more volatile than Gamestop shares. However, for all its misgivings, audiences still capitalize web3, with prices far from zero. Parallel, a new web3 CCG hit a half-billion market cap considering token and NFT prices, and yes, it’s pre-launch. Despite flaws, Parallel looks cool, and games like Sipher are turning heads, while Sorare is already established. Chris Heatherly is brewing something with Mystery Society, giving ‘Among Us live-service’ a jolt. But for all its hopes, web3 has been blocked by distribution and confined to the browser. Epic Game Store, a trusted brand, now carries web3 games, even with an Adults Only rating. Finally, Web3 is playable on mobile, with the compromise of giving Apple 30% and tacking on an equivalent user-facing tax. All this festers into 2024 as the year web3 ships a chart-topping product; it can’t keep failing upward. Right?

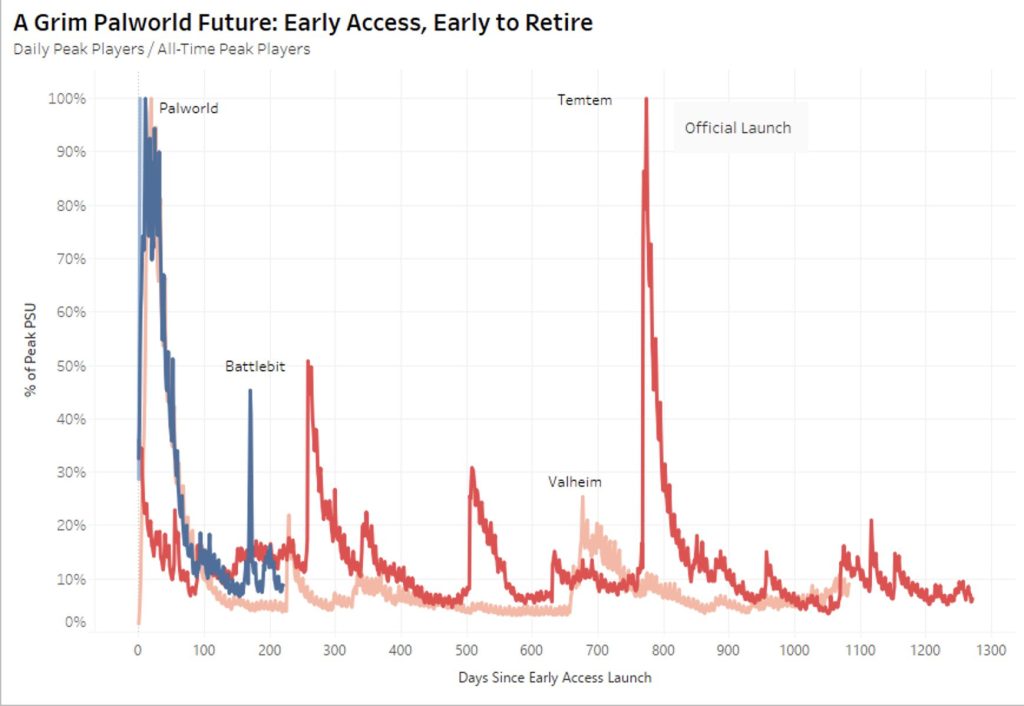

After four days, Palworld, an early-access survivor game described as “Pokemon with guns,” grossed ~$108M over three days en route to the 2nd highest concurrent player count for a paid title on Steam. It’s an outstanding success for Pocket Pair, a 50-person Japanese team with $7m raised. But like early access hits Valhiem, Battlebit, and Temtem before it, an inability to quickly deploy capital hampers compounding return. Instead of these titles having their best days to look forward to, they’re in the rear-view mirror, the equivalent of peaking in high school, but this time, you get millions in cash for the ordeal. Teams should follow the Kikta Studio model: prove a trajectory and let someone else build the bow. When founders sell games, they retain control of their destiny and find themselves newly rich with modelable capital, allowing games to grow into their best selves.

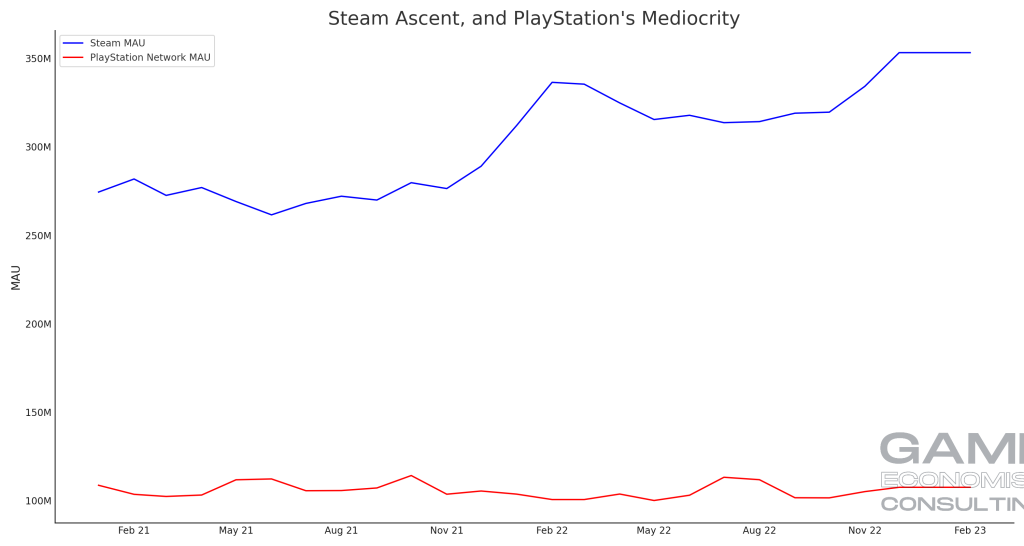

Imsominaic leaks reveal Playstation lost 3M MAU over the last three years. At a time when gaming is at its grandest heights, consoles have failed to seize the moment. Sony and Microsoft have forgotten their role as platforms, purchasing dead-end franchises instead of fostering third-party innovation. Meanwhile, Steam gained over 90M users, a ~35% increase over the same period, with Valve founder Gabe Newell downing New Zealand pies as third-party development rakes in billions as Valve barely lifts a finger.

subscribe to the blog subscribe to the blog subscribe to the blog subscribe to the blog subscribe to the blog subscribe to the blog subscribe to the blog subscribe to the blog